Work to live: Break the debt cycle

This post may contain affiliate links. Click here to see what that means.

My husband said not to long ago that, “If I wasn’t married to you, I’d be driving a Jeep.” At first, I wasn’t sure how to take that. Was it a criticism? Or was he testing the midlife crisis waters to see if he could buy one?

So, being the good wife that I am, I asked, “What does that mean?”

His reply (obviously in my favor, or I’d never blog about it) was, “I would have kept spending on the things I want right now, like a fully loaded Jeep. I’d be in debt up to my eyeballs. I’d also be living to work to pay all those bills. Because of you, we will actually retire one day.” Then he smiled, that sweet smile with the twinkle in his eye that made me fall in love back in the seventh grade, and said, “But I still want a Jeep one day.”

Live to work or work to live?

To “live to work” means your life is all about the work — whether because you like working or because you enjoy keeping score. You’ve heard deathbed stories where people say if they could do it all over again, they’d work less and live more. Those who live to work prioritize work over other things.

On the other hand, those who “work to live” balance the pursuit of income with other interests. More focused on the living, they prioritize time off from work to have time for things they enjoy, like family and hobbies.

My husband, without my frugal input, would spend more and have to work harder to pay for those “toys.” But, as we define life goals together, he has more balance. No Jeep (yet), but more balance.

For our family, life outside work is more important than amassing great wealth. That family time affects every decision we make, including which car to buy. In all, we have found a balance that allows us some luxuries, like travel, without dedicating every waking minute to work. We spend weekends together, playing games, watching movies and cooking. My husband gets home in time for family dinner almost every night. Our work-life balance tips in favor of life over wealth.

Eliminate debt for better work-life balance

To maintain our work-life balance, we had to eliminate debt. My husband graduated in 1993 with $130,000 in student loans. That’s a lot of debt for a young couple. For several years, we made regular payments — doing nothing to aggressively pay the debt down. One day years ago, my brother (who works in the financial industry) asked why we weren’t paying the debt down quicker, instead of flushing all that interest “down the toilet.” Hmmmm! Good question!

His question inspired us to make changes. We cut back on our everyday expenses and started adding additional principal to each student loan payment. Amazingly, what would have taken 30 years to repay was paid in full in only 17 years! We saved thousands in interest — which meant my husband’s income went more toward life and less toward bills. This one change made a huge difference in our work-life balance.

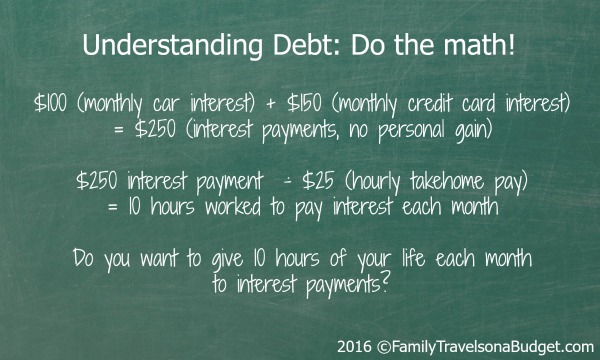

Do the math

Imagine this: All the interest you pay is money going toward nothing. You have to work a specific number of hours just to pay that debt without any personal gain.

Example: You earn $25/hour (let’s assume no health insurance, social security or income tax — this is your actual take home pay per hour). You have a car payment and credit card balance. Let’s say you pay $100 in interest on the car and $150 in interest on the credit card each month, for a total of $250 per month. To make those interest payments, you have to work 10 hours each month!

If you don’t have that debt, that $250 is all yours to do whatever you want. Travel, anyone?

What I’m trying to say….

Bottom line here… People who want more family time, whether to vacation or just have dinner at the table together, need to make financial choices to achieve those goals.

While my husband wants a Jeep, he realizes that fulfilling that personal dream (right now) would sacrifice our family dreams. I am thankful we work together to achieve all our dreams.

Yes, we make room in the budget for things we want individually — we just started setting aside money for his dream of a Jeep Rubicon. When we have the money, he will have it! We choose to put family goals first and personal goals second. And our family goals begin with making sure our budget doesn’t dictate how we spend our free time. HAVING to work because of debt is not how we want to live — ever!

As I find cool budgeting tools, I’ll share them here or on Facebook.

What’s your take on the live to work vs. work to live balance? Is there a particular area where you struggle? Do you have a success story? I’d love to know.

[amazon_link asins=’1986519228,1985217996,1284118215,1978203241,1530187028′ template=’ProductCarousel’ store=’ftoab-20′ marketplace=’US’ link_id=’37ee8908-ec6d-11e8-ad93-d94bf7b4876b’]